I Fell Down a Weird Rabbit Hole (And What I Found Is Wild)

%20copy.png)

Today at a Glance

- One of the fastest-growing business models in America isn’t tech — it’s law

- ~95% of cases settle, turning litigation into a math problem

- 30–40%+ referral fees reward case sourcing over trials

- Massive ad spend fuels the machine

- Insurance costs rise — businesses and consumers pay

Over the last few weeks, I’ve gone deep on personal injury + employment law firms.

What I found is honestly insane.

They’re not just lawyers (if you can even call them that).

They are:

- One of the fastest-growing types of businesses in the country

- One of the largest advertisers in the country

- And the entire industry runs on a brutally simple economic equation:

Cost of settling vs. cost of going to trial

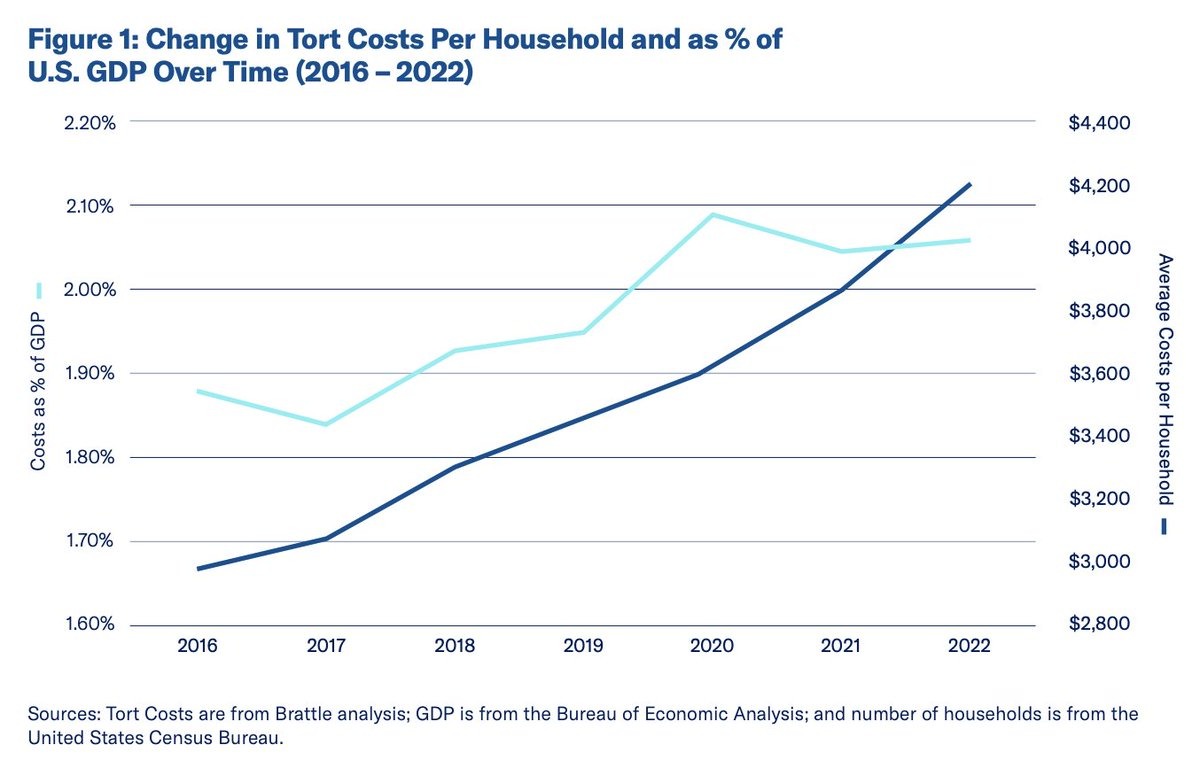

"Costs and compensation paid in the U.S. tort system reached over $529 billion in 2022, or over $4,200 per U.S. household." That’s roughly 2% of U.S. GDP.

Every billboard, TV ad, and Google search exists to feed cases into a system that exploits that math.

And here’s the stat that explains everything:

~95% of personal injury and employment cases never go to trial.

They settle.

The entire industry is one big bet on getting companies — and more importantly, insurance providers — to pay to make claims go away.

The Hidden Tax on Businesses

This model isn’t just reshaping law.

It’s reshaping the cost of doing business in America.

When litigation risk rises, insurers don’t absorb it.

They raise prices.

Over the last several years, business insurance premiums have increased quarter after quarter (reports show 29 consecutive quarterly increases), driven by:

- Larger settlements

- Higher claim frequency

- What insurers openly call “legal system abuse” or “social inflation”

The result:

- Higher insurance premiums (5-7% uplift each renewal)

- Higher operating costs

- Higher prices passed directly to consumers

In states like California, the risk has become so asymmetric that some large companies:

- Will not hire employees in who live in California

- Or refuse to operate there entirely

Legal exposure becomes a massive shadow tax on growth.

The Fastest-Growing Advertisers (In Plain Sight)

Follow the money.

Personal injury and employment law firms are now:

- Among the largest advertisers in the country

- The #1 buyers of out-of-home advertising (billboards, buses, benches)

- Massive spenders across Google Search, TV, YouTube, and radio

Firms like Morgan & Morgan spend hundreds of millions per year on advertising alone.

They flood markets.

Why?

Because once you control intake, everything downstream becomes leverage.

The Business Model (It’s a Referral & Commission Machine)

At a high level, the model looks like this:

- Buy attention at scale

- Convert calls through intake and call centers

- Qualify cases quickly

- Route cases (keep, refer, or co-counsel)

- Push execution downstream

What looks like a law firm is often just:

- A marketing engine

- An outsourced intake center

- A referral network of attorneys

- A mathematical settlement structure

The actual legal work is modular. Most all of these “claims” are copy, paste, file. They just swap out the plaintiff's and defendant’s names.

Distribution is the moat.

The Referral Model Is the Real Cheat Code

Here’s the part most people don’t realize:

Only attorneys can legally charge referral fees that take a percentage-based commission of the settlement. (If you aren’t a licensed attorney, you can only charge flat rate referral fees.)

And those fees are meaningful.

Referral fees commonly range from 30% to 40%+ of the attorney recovery.

Combine that with the fact that ~95% of cases settle, and you get a volume-driven settlement machine optimized for routing, not trials.

The Math That Explains the Entire Industry

Let’s walk through a simple example.

A $100,000 Settlement

Step 1: The Case Is Sourced

- Attorney A markets aggressively and sources the case.

- Attorney A qualifies the lead, then refers the case to Attorney B, who files the lawsuit.

Step 2: The Case Settles

- Like the vast majority of cases, it settles before trial.

- Total settlement amount: $100,000

Step 3: The Money Flows

Referring Attorney (Attorney A)

- Receives a 30–40% referral fee (as a percentage of the attorney recovery)

- Can earn $10,000–$15,000+ for sourcing the case alone

Litigating Attorney (Attorney B)

- Recovers 100% of case expenses first (filing fees, experts, discovery)

- Then earns their own 30–40% contingency fee

Plaintiff

- Receives the remainder after:

- Expenses

- Contingency fees

- Referral fees

- Expenses

No trial.

No verdict.

Just math.

Multiply this by thousands of cases per year, and the business model becomes obvious.

Morgan & Morgan: The Billionaire Factory

Morgan & Morgan isn’t really a law firm.

It’s a national media company with a legal backend.

They didn’t out-litigate the market.

They out-distributed it.

Control intake → control settlements → control outcomes.

That’s how they’ve minted billionaire attorneys.

The Wild Part: Tiny “Firms” Printing Money

Here’s what really blew my mind.

I’ve personally spoken with an attorney making $10M+ per year with this model:

- He’s the 1 licensed attorney

- He has a contract marketing team

- An outsourced call center

- A fleet of offshore contractor paralegals

- A referral and co-counsel network

No fancy offices.

Virtually zero headcount.

Just leverage.

The Real Insight

This isn’t really about law.

It’s about:

- Asymmetric risk

- Regulation-created moats

- Media-driven distribution

- And a system optimized around settlement math

Whenever you see:

- High downside for businesses

- Insurance as the real payer

- And an equation that favors “pay to make it go away”

You get an industry that behaves more like:

Media + Finance + Insurance

Most people never notice.

They just pay higher prices.

Subscribe to

Get one powerful growth playbook, every Saturday morning.

Related Articles

One powerful growth playbook, delivered every Saturday morning